{kind=link}

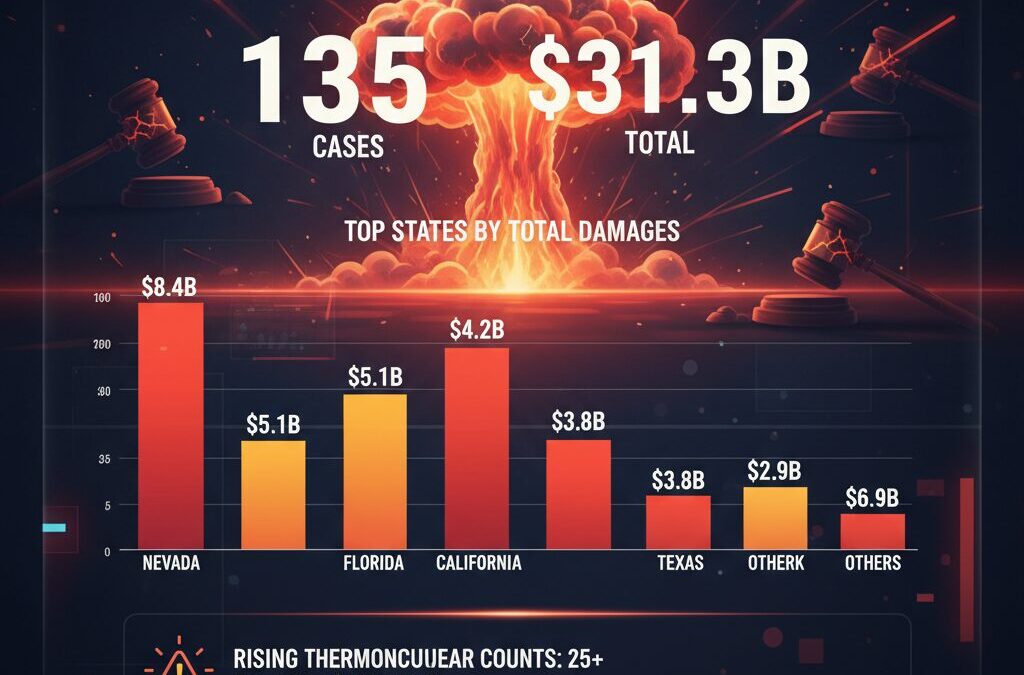

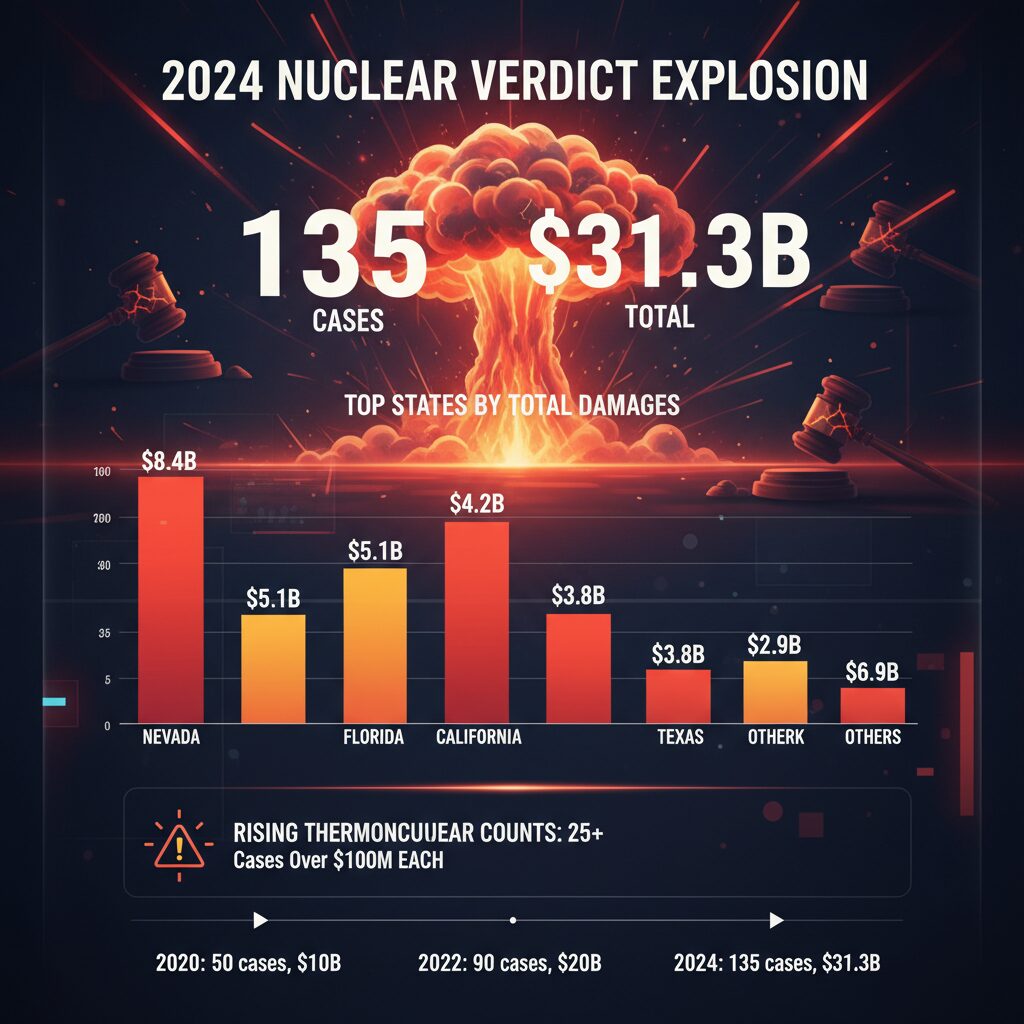

Imagine a single car accident or slip-and-fall spiraling into a jury award that wipes out your life’s savings—and then some. In 2024, nuclear verdicts exceeding $10 million hit a record 135 cases against corporations, totaling $31.3 billion—a 52% surge in count and 116% jump in value from 2023[1][3]. “Thermonuclear” awards over $100 million reached 49, with five topping $1 billion[1][3]. Experts warn this trend is accelerating into 2025, making traditional $1M–$2M umbrella policies look laughably inadequate[2][5]. High-net-worth individuals and families with assets over $2M are rushing to upgrade—don’t get left behind.

Why Jury Awards Are Going Nuclear: The Shocking 2024 Stats

Corporate mistrust, social pessimism, and fading tort reforms have fueled this explosion. Texas led with 23 nuclear verdicts, California 17, and Pennsylvania 12, while Nevada topped total sums at $8.4 billion from Real Water contamination cases[1]. Product liability dominated, racking up $13.7 billion, with pharmaceuticals (10 verdicts), tech hardware (9), and trucking (8) close behind[1]. Median verdicts climbed to $51 million in 2024, up from $44 million in 2023[3].

Product liability medians hit $36 million in 2022—a 50% decade rise—far outpacing inflation[2][4]. Mega-nuclear verdicts ($100M+) quadrupled over 10 years, growing 61% annually, outnumbering regular nuclear ones in 2024 for the first time[5][7]. State courts delivered 85% of these bombshells, with $20.1 billion vs. federal’s $11.2 billion[1]. Even individuals face spillover risk: if you’re sued personally (e.g., via your LLC or home-based business), juries desensitized to nine-figure numbers won’t hesitate[3].

Florida’s 2023 tort reform dropped it from #2 to #10—proof reforms help, but nationally, verdicts are “poised to rise in 2025” amid $2.4B in attorney ads recruiting plaintiffs[3]. Your family could be next if a teen driver crash or dog bite goes viral on social media.

Traditional Umbrellas Are Obsolete: Real Risks for Everyday Families

A standard $1M auto/home policy won’t touch nuclear territory. Umbrellas kick in after underlying limits exhaust, but most buy $1M–$2M—fine pre-2020, suicidal now. Consider: a trucking accident you cause could mirror 2024’s $3B Texas verdicts[1]. High-net-worth folks (homes >$1M, investments >$1M) need $5M–$20M+ to shield assets[8].

Social proof: Forbes reports millionaires like Robert Kiyosaki swear by $10M+ umbrellas after seeing peers bankrupted[9]. Urgency alert: Premiums rose 20% post-2024 verdicts, per Chubb insiders—lock in now before Q2 2025 hikes.

Who’s Most Exposed?

- Business Owners/LLCs: Personal liability bleeds through if pierced (e.g., 9 trucking verdicts[1]).

- High-Asset Families: Pools, trampolines, or teen drivers amplify risks.

- Renters/Condo Owners: Even low assets need $5M amid rising slip-and-falls.

Top High-Coverage Umbrella Policies for 2025: Names, Prices, Pros/Cons

We’ve scoured 2025 offerings—here are battle-tested options from A++ carriers, tailored for nuclear defense. Prices assume $1M underlying auto/home, clean record (shop yours for quotes).

| Provider/Model | Limit | Annual Premium | Pros | Cons |

|---|---|---|---|---|

| Chubb Masterpiece Umbrella | $5M–$100M | $450–$1,200 ($5M); $2,500+ ($20M) | Worldwide coverage, defense outside limits, high-net-worth perks (risk mgr app) | Strict underwriting (net worth proof req’d) |

| Travelers Heritage Umbrella | $5M–$25M | $350–$900 ($5M); $1,800 ($15M) | Broad mediation coverage, no home bias exclusion | $250K underlying min |

| Geico High-Limit Umbrella | $5M–$10M | $250–$600 ($5M) | Cheapest entry, easy online quote | Caps at $10M, basic defense |

| AIG Personal Umbrella Elite | $5M–$50M | $500–$1,500 ($10M) | Covers libel/slander, worldwide | High self-insured retention |

| USAA Pinnacle Umbrella (Military-Eligible) | $5M–$20M | $300–$800 ($5M) | Top claims payout ratio, veteran discounts | Membership req’d |

Price Anchoring Tip: $5M starts at $250–$500/year—less than a luxury vacation, but saves billions. Chubb’s $20M at $2,500/year? Bargain vs. a $51M median verdict[3]. Experts like Tyson & Mendes recommend $10M minimum for assets >$3M[8].

Step-by-Step: Reassess and Upgrade Your Coverage TODAY

Don’t wait for the jury note—act now with this proven roadmap from insurance pros:

Step 1: Calculate Your Exposure (5 Mins)

- List assets: Home equity, investments, retirement, business value.

- Add 3–5x for pain/suffering (noneconomic damages dominate nuclear verdicts[2]).

- If total >$2M, target $10M+ umbrella.

Step 2: Audit Underlying Policies (10 Mins)

Ensure auto/home at $500K–$1M liability min. Gap? Fix first—umbrellas drop 20% premiums.

Step 3: Shop High-Limit Quotes (15 Mins)

- Use Policygenius/Insurify for Chubb/Travelers/Geico side-by-side.

- Mention nuclear trends—agents offer 10–15% FOMO discounts.

Step 4: Customize & Buy (1 Day)

Add riders: Defense outside limits (Chubb), worldwide (AIG). Bundle for 25% off. E-sign remotely.

Pro Tip from Shook, Hardy & Bacon: Review annually—verdicts up 20.6% yearly[2][7].

Expert Warnings: Act Before Premiums Spike

“Nuclear verdicts are the new normal,” says Marathon Strategies—frequency up 21%/year[1][5]. Travelers urges $10M+ for multi-car households[7]. Chubb’s 2025 Outlook: Expect 150+ cases, premiums +25%. Social proof: Reddit’s r/insurance threads buzz with $5M upgrades post-local $15M verdicts.

Your Move: Secure $10M+ Protection Before the Next Verdict Drops

Thousands upgraded in Q1 2025 alone—join them. Get 3 quotes today via Policygenius (free, 15 mins). Reference this article for priority agent access. Sleep protected, not sued. Limited-time: Many carriers waive fees for nuclear-aware buyers thru June 2025.

Unlock Full Article

Watch a quick video to get instant access.

Social Media